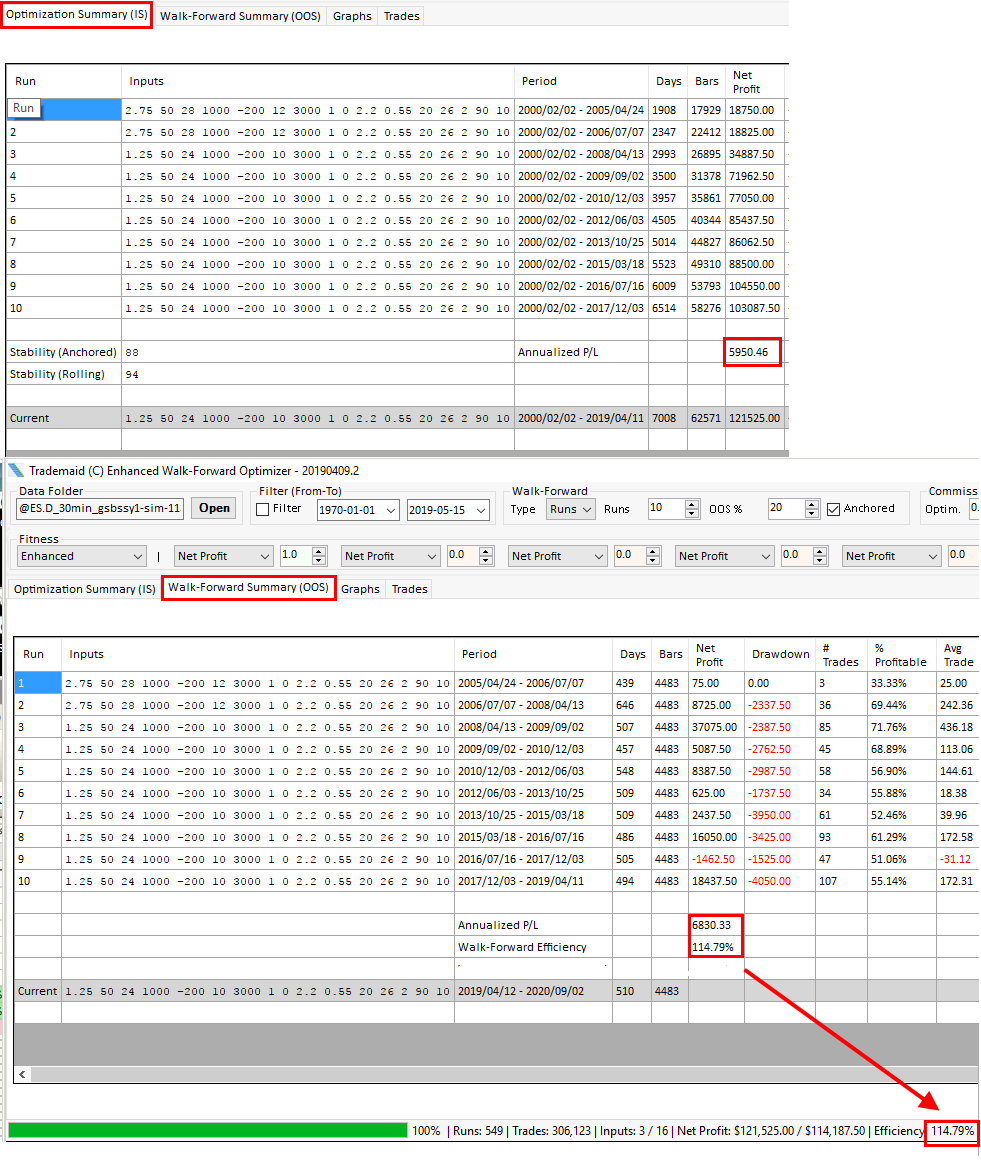

Walk-forward efficiency

This is the annualized rates of return for the out-of-sample results divided by the in-sample results. This is considered a metric for measuring the trading system's robustness.

See picture below for how it is calculated.

Modified on: Sun, 29 Sep, 2019 at 6:39 PM

This is the annualized rates of return for the out-of-sample results divided by the in-sample results. This is considered a metric for measuring the trading system's robustness.

See picture below for how it is calculated.

Did you find it helpful? Yes No

Send feedback